Conservation easements place permanent restrictions on division of land.

.

.

.

.

.

.

.

.

.

Donations of conservation easements offer tax benefits to landowners.

.

.

.

.

.

.

.

.

.

Determining the value of a conservation easement.

.

.

.

.

.

.

Federal tax deduction.

.

.

.

.

.

.

State of Colorado tax credits.

.

.

.

.

.

.

.

.

.

.

.

.

End of the Colorado tax credit program.

.

.

.

.

.

.

.

.

.

.

.

Interaction of federal tax deduction and state tax credits.

.

.

.

.

.

.

.

.

.

Property tax assessment (agricultural).

.

.

.

.

.

.

.

.

.

.

.

.

Conservation easements require legal and technical documentation.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

.

Grants are available for conservation easements.

.

.

.

.

.

.

.

.

.

.

.

.

Conservation easement donation example.

Conservation Easement Details

A conservation easement is a legal agreement between a landowner and a qualified conservation organization, usually a land trust, that permanently limits uses of a property to protect its conservation values. It is one of the most powerful and effective tools available for the permanent protection of private land while leaving it in private ownership. Conservation easements are perpetual. They are recorded with the county clerk and run with the land.

At its most fundamental level, a conservation easement prohibits subdivision and development, maintaining the conservation values of open space, agricultural productivity, scenic vistas and wildlife habitat. Landowners retain title to their land and continue to use, manage and enjoy it, subject to the terms of the easement.

A conservation easement does not grant public access to a property unless the landowner specifically chooses to grant access. An easement also does not prevent a landowner from mortgaging, leasing, selling or passing on their land. In fact, a conservation easement can be a great tool for families who wish to keep land intact for the next generation.

_________________________________________________________

The donation of a conservation easement is governed by the charitable contributions section of the IRS tax code. To qualify for tax benefits, property receiving a conservation easement must meet at least one of four conditions:

- Preservation of land for outdoor recreation by, or education of, the general public.

- Protection of relatively natural habitat for fish, wildlife, or plants, or a similar ecosystem.

- Preservation of open space (including agricultural and forest land) either for the scenic enjoyment of or significant benefit to the general public.

- Preservation of historically important land or structure.

Most property in Western Colorado qualifies under the second and third categories, providing relatively natural habitat for wildlife and preserving agricultural or forested open space.

_________________________________________________________

In giving up the development potential of the land by placing a conservation easement, the fair market value of the property is reduced. The reduction in fair market value is considered to be a charitable contribution. The amount of the contribution is determined by a qualified appraisal that compares the value of the property without the conservation restrictions to its value subject to the restrictions. The difference between the “before” and “after” values is the value of the conservation easement. It is a measure of what is voluntarily given up by placing the conservation easement on the property. Only actual sales of comparable properties in the same or similar geographic area are to be considered by the appraiser in determining the “before” and “after” values.

_________________________________________________________

If a conservation easement satisfies the Internal Revenue Code requirements, then the grantor of a conservation easement is eligible for a charitable income tax deduction for the value of the conservation easement. This charitable tax deduction qualifies the landowner for a 50% reduction in adjusted gross income for the year of the conservation easement donation and up to 15 years forward. If the donor’s gross sales are 50% or more from agriculture, the donation generates a 100% deduction for up to 16 years.

_________________________________________________________

The donation of a conservation easement also qualifies a landowner for a Colorado state tax credit. The tax credits are administered by the State Division of Conservation through an application process after the conservation easement donation is made. The Division has 120 days to review the application before issuing the tax credit certificate that allows the donor of the easement to claim a tax credit on their state income tax. The tax credit is a dollar-for-dollar reduction of state income tax liability.

Colorado tax credits are good for up to 20 years. Tax credits are transferable and can be sold for cash on the open market through tax credit brokers. The rate fluctuates, but currently a landowner could expect to sell tax credits at approximately 85% of their value.

Through 2026, the state tax credit equals 90% of the donated value of the conservation easement. For conservation easements donated in 2027 through 2031, tax credit certificates will be issued for 80% of the donated value. A maximum of $1.5 million can be claimed in any single year. The remainder may be carried over to future years, up to a maximum tax credit of $5 million per conservation easement.

_________________________________________________________

As of March 10, 2026, the carryover of tax credit applications to future years means that approved tax credit applications are receiving 2030 tax credits. Soon the 3031 credits will be reserved, definitely before the end of 2026.

Once the $50 million cap for 2031 is claimed, no more tax credits are available. For example, if the last tax credits for 2031 tax credits are gone as of 7/31/26, conservation easements that close after that date will not receive a tax credit under current law.

A bill has been submitted to the legislature to extend tax credits through the year 2036, but with no changes to keep from perpetuating the early reservation of each year’s tax credit cap. If the bill passes, it will be possible for the 2036 tax credits to be claimed years before, again resulting in the possibility of donating a conservation easement with no state tax credit benefit.

The CO Division of Conservation website maintains a running total of tax credit amounts that have been reserved for each tax year at https://conservation.colorado.gov.

_________________________________________________________

Under current federal tax law relating to charitable contributions, the federal deduction for the donation of a conservation easement is reduced by the value of any state tax credit.

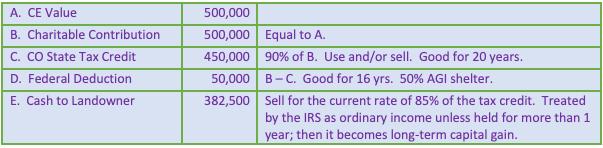

For example, a conservation easement valued at $500,000 can generate a charitable contribution of $500,000, usable as described above. However, if the landowner also claims a Colorado state tax credit for the conservation easement donation, which would be $450,000 (90% of 500,000), the federal charitable contribution would be reduced to $50,000 (500,000-450,000).

Depending on each landowner’s tax situation, it may be beneficial to forego seeking a state tax credit. The reduction in the federal deduction happens immediately that a state tax credit is approved, independent of how the landowner uses or sells that tax credit. As in all cases relating to taxes, professional advice from a CPA experienced in these matters is essential.

_________________________________________________________

As a result of placing a conservation easement, Colorado Revised Statutes (§ 39-1-102(1.6)(a)(I)(A), C.R.S.) allows for determination of agricultural land assessment if it meets the following criteria:

“A parcel of land that consists of at least 80 acres, or less than 80 acres if the parcel does not contain any residential improvements, is subject to a perpetual conservation easement. The area is classified by the assessor as agricultural land at the time the easement was granted, if the easement was to a qualified organization, or if the easement was granted exclusively for conservation purposes, and if all current and contemplated future uses of the land are described in the conservation easement. This provision does not include any portion of such land that is actually used for non-agricultural commercial or residential purposes.”

All conservation easements resulting from GRCL’s work meet the criteria listed above. The conservation easement will be granted to qualified organizations (land trusts) exclusively for conservation purposes, and all current and future uses will be described in the conservation easement.

_________________________________________________________

A conservation easement is a deeded real estate transaction that requires legal and technical documentation. Each project requires the following before the transaction can be completed:

- A specialized appraisal that determines the conservation easement value of the property.

- A baseline inventory report that documents the present condition of the property.

- A geological report that documents the likelihood of mineral extraction on the property through surface disturbance (not necessary if 100% of minerals are owned by the landowner).

- A water rights report documenting the status of any water rights included with the conservation easement.

- Creation of the deed of conservation easement, including legal review of easement language.

- Title work and closing costs.

- A stewardship endowment for the land trust that enables them to monitor the conservation easement on the property in perpetuity.

In 2026, total transaction costs associated with completing a conservation easement are estimated at $105,000 and above. Properties located in Gunnison County are eligible for grant funding to pay these expenses. As a service, GRCL seeks grant funding for from the Gunnison County Land Preservation Fund if landowners would like the financial assistance. For properties located outside of Gunnison County, land trusts sometimes offer to seek other grants or provide zero-interest loans to cover these costs.

_________________________________________________________

Since 1995, GRCL has worked to secure grants to compensate landowners for up to 75% of the value of their conservation easement. Appraisers and other professionals call this a “bargain sale,” wherein the property owner voluntarily accepts less than 100% of the value of the property being sold (the conservation easement).

The process for placing a grant-funded conservation easement is similar to that of donating a conservation easement, with the possible addition of some terms specified by the funding source, and also a review process that incorporates the funding source’s requirements. The grant amount is paid to the landowner at the closing of the conservation easement.

The value of the conservation easement that is not covered by the grant amount is considered a charitable donation. Using the example above, a grant might provide 75% of the CE value, or 375,000 (.75 x 500,000). The donation would be 125,000. The calculations for federal and state tax benefits would be as shown in the example, substituting 125,000 as the charitable contribution in Item B. Note that conservation easement grant income is treated as capital gains, and therefore can be eligible for 1031 “like kind” exchanges if desired.

_________________________________________________________

The value of a CE is the result of a subtraction problem. First the appraiser must consider what the entire property is worth before the CE is placed. This is called the “before” or “unencumbered value.” It is a wholesale number: i.e. what would a buyer pay for 320 acres in one purchase?

Then the appraiser must estimate what a buyer would pay for the property with the CE attached, which means the property is now 320 acres as one parcel forever, most likely with a headquarters area for residential and agricultural buildings. This is called the “after” or “encumbered” value. The value of the CE is the difference between the two numbers.

Assume that the CE appraiser says that the property is worth $1,500,000 before the CE and $1,000,000 after the CE is placed. Here is a calculation of the CE value, based on these assumptions:

Unencumbered Value (before CE) = 1,500,000

Encumbered Value (after CE) = 1,000,000

CE Value = 500,000

Table 1: Financial Benefits if Claiming a CO State Tax Credit

Table 2: Financial Benefits (Federal Deduction Only)

Note: This information is offered with the understanding that neither the Gunnison Ranchland Conservation Legacy nor the writer are engaged in rendering legal, accounting, or tax advice or service. If such advice or expert assistance is required, the services of experienced professional advisors should be sought.